Navigating the Prescription Drug Puzzle: An In-Depth Guide to Understanding Medicare Part D

- Paula White

- Dec 19, 2023

- 3 min read

In this comprehensive guide, we look at the complicated world of Medicare Part D, investigating its key features, the penalties incurred for delayed enrollment, the impact of IRMAA premiums, and emphasizing the pivotal role of annual plan reviews.

What is Medicare Part D?

Medicare Part D, a pivotal component of the broader Medicare program, was implemented in 2006. This voluntary program represents a collaborative effort between the federal government and private insurance companies approved by Medicare.

Its primary objective is to alleviate the financial burden of prescription drug costs for beneficiaries.

Key Components of Medicare Part D

Monthly Premiums

Part D plans require beneficiaries to contribute a monthly premium, varying across plans. Delving the available options becomes paramount to identifying a plan that aligns with your budget and prescription needs.

Formularies and Tiers

Integral to Part D plans is the formulary, a comprehensive list of covered medications and their associated costs. Annual reviews of the formulary are crucial for beneficiaries to ensure that their required medications remain covered.

You should always consider what tier your medication falls under since a lower-tiered designation will usually be covered more favorably than a higher-tiered one.

Deductibles

Before the Part D coverage commences, beneficiaries usually must fulfill a deductible—a predetermined out-of-pocket amount. This is the threshold that must be met before the plan initiates cost-sharing.

Initial Coverage Phase

Once your deductible is met (if applicable), the Part D drug plan begins to cover some of the prescription drug costs.

Coverage Gap (Donut Hole)

The coverage gap, colloquially referred to as the "donut hole," is the phase where beneficiaries face increased out-of-pocket costs.

Catastrophic Coverage

Beneficiaries transition into the catastrophic coverage phase once out-of-pocket spending surpasses a predefined threshold. During this stage, they are not responsible for any coinsurance or copayment for covered drugs.

What Are IRMAA Premiums?

The Income-Related Monthly Adjustment Amount (IRMAA) may apply to some higher-income beneficiaries. This means that an extra amount is added in addition to the regular Part D premium.

High-income earners must know these additional costs, as they are determined based on the modified adjusted gross income reported to the IRS.

Choosing the Right Plan

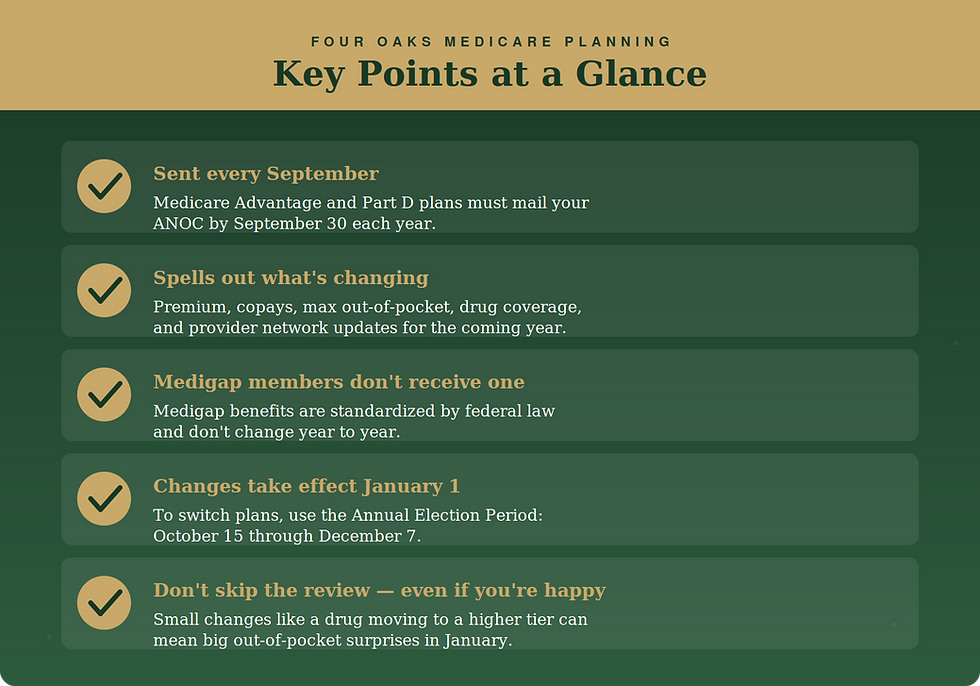

Selecting an optimal Part D plan involves a multifaceted evaluation, considering factors such as medication needs, cost structures, and preferred pharmacy networks. Given the dynamic nature of Part D plans, beneficiaries must revisit these considerations annually during the annual election period.

Enrollment and Open Enrollment

Navigating the world of Medicare Part D necessitates understanding specific enrollment periods. The Initial Enrollment Period, commencing three months before turning 65 and extending for seven months, offers a window for individuals to enroll.

Equally important is the Annual Election Period, occurring from October 15 to December 7, providing an opportunity for beneficiaries to review and modify their Part D coverage for the upcoming year.

Late Enrollment Penalties

Delaying enrollment in Medicare Part D may have financial repercussions if you do not have other credible coverage for Part D. Premium penalties and coverage gap impacts underscore the urgency of timely enrollment, making it a priority for prospective beneficiaries.

The Dynamic Nature of Part D Plans

Part D plans undergo annual adjustments, including alterations to premiums, formularies, tiers, and preferred pharmacy networks. Beneficiaries must be cognizant that the plan aligning with their needs in one year may necessitate reconsideration in the following year.

Do You Have to Get a Part D Plan?

While enrolling in a Part D plan is generally advisable, some beneficiaries may wonder if it's mandatory. The answer depends on various factors, including whether they have alternative creditable prescription drug coverage—failure to enroll when first eligible may result in late enrollment penalties.

Avoiding Penalties and Staying Informed

To navigate the intricate landscape of Part D effectively, beneficiaries are advised to enroll during the Initial Enrollment Period and use the Annual Election Period for comprehensive plan reviews and potential adjustments. Regular reviews, staying informed about plan updates, and qualifying for Special Enrollment Periods when applicable contribute to a seamless and cost-effective healthcare experience.

Understanding Medicare Part D, comprehending the penalties associated with delayed enrollment, recognizing the impact of IRMAA premiums, and acknowledging the differences within plans are important for informed decision-making.

By navigating the complexities of Part D, staying proactive during enrollment periods, and conducting regular plan reviews, beneficiaries can ensure access to affordable prescription medications tailored to their changing healthcare needs. If you need help in your navigation, give us a call. We'll walk you through the process free-of-charge.

Comments