Medicare Advantage vs. Medigap Plans: The Two Roads of Medicare

- Paula White

- Dec 19, 2023

- 3 min read

Updated: Dec 27, 2023

As individuals approach the age of 65, they are faced with a critical decision that will significantly impact their healthcare coverage – choosing between Medicare Advantage and Medigap plans.

Medicare, the federal health insurance program for individuals aged 65 and older, provides essential coverage, but there are gaps that beneficiaries often need to fill. This is where Medicare Advantage and Medigap plans come into play, each offering unique features and considerations.

What is Medicare?

Before delving into the decision-making process, it's crucial to have a basic understanding of Medicare.

Medicare is divided into four parts:

Part A (Hospital Insurance): Covers inpatient hospital stays, hospice care, and some home health care.

Part B (Medical Insurance): Covers outpatient care, doctor visits, preventive services, and some home health care.

Part C (Medicare Advantage): An alternative to Original Medicare, Part C combines Part A and Part B coverage and often includes additional benefits such as dental and vision.

Part D (Prescription Drug Coverage): Provides prescription drug coverage through private insurance plans.

What to Know About Medicare Advantage (Part C)

Pros

Comprehensive Coverage: Medicare Advantage plans often include coverage for vision, dental, and hearing, which Original Medicare does not cover.

Cost Containment: Many Advantage plans have out-of-pocket maximums, limiting the annual costs beneficiaries may incur.

Convenience: Private insurers typically offer Part C plans and can simplify healthcare by combining coverage into one plan.

Cons

Network Limitations: Advantage plans may have a restricted network of healthcare providers, limiting choices.

Referral Requirements: Some plans may require referrals to see specialists, adding an extra layer of bureaucracy.

Geographical Restrictions: Coverage may be limited to specific regions, affecting those who travel frequently or reside in multiple locations.

What to Know About Medigap or Medicare Supplement

Pros

Freedom of Choice: Medigap plans allow beneficiaries to visit any healthcare provider that accepts Medicare.

Predictable Costs: Medigap plans help fill the gaps in Original Medicare, providing more predictable out-of-pocket costs.

No Network Restrictions: With Medigap, there are no network restrictions, making it easier for beneficiaries to access care nationwide.

Cons

Higher Premiums: Medigap plans generally have higher monthly premiums than Medicare Advantage plans.

No Prescription Drug Coverage: Medigap plans do not cover prescription drugs, necessitating the purchase of a separate Part D plan.

No Dental, Routine Vision, or Hearing Coverages: While Medigap plans to cover certain out-of-pocket costs, they may not include additional benefits like dental, vision, and hearing coverage.

Additional Considerations

Healthcare Needs

Consider your current health status and any anticipated healthcare needs. If you require specialized care or regular prescriptions, evaluate how each plan meets those needs.

Budget Constraints

Assess your budget to determine which plan aligns with your financial situation. While Medigap plans may have higher premiums, they often result in lower out-of-pocket costs.

Preferred Providers

If you have specific healthcare providers you prefer, check if they are in the network of your chosen plan. This is particularly important for Medicare Advantage beneficiaries.

Geographic Flexibility

Consider your lifestyle and whether you need a plan with nationwide coverage. Medigap plans generally offer more flexibility in choosing healthcare providers across the country.

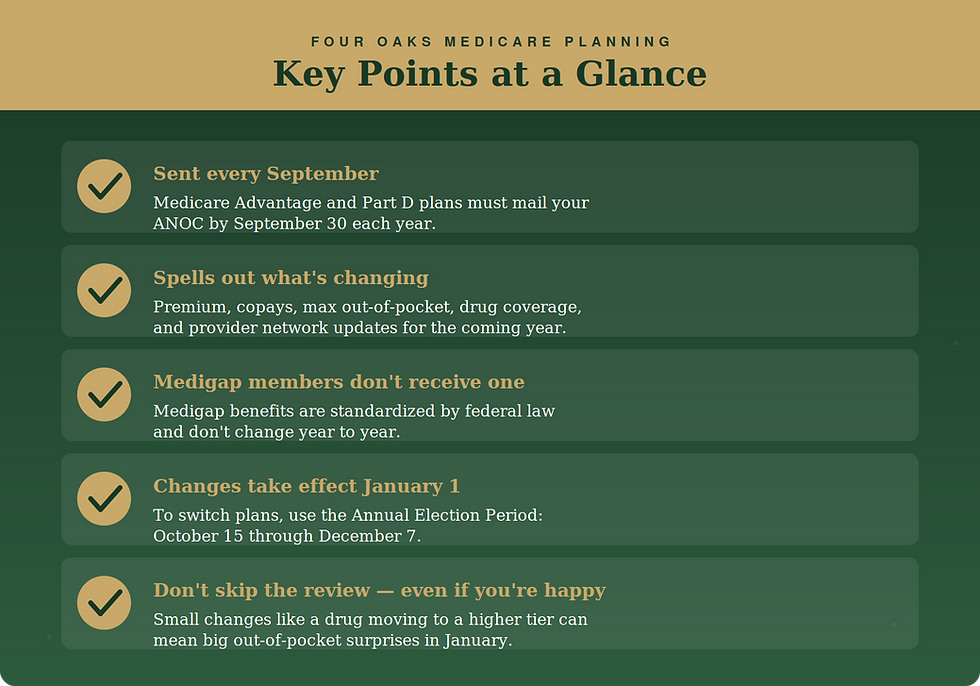

When you are going onto Medicare Part B for the first time, a company cannot deny you a Medigap plan based on your health (i.e., there are no underwriting questions). This is called the Medicare Supplement Open Enrollment period, which only lasts six months, starting the first month your Part B is effective.

Rely on a Trusted Medicare Partner in Austin, TX

Choosing between Medicare Advantage and Medigap plans is a personal decision that depends on individual healthcare needs, budget constraints, and lifestyle preferences. It's essential to carefully evaluate the pros and cons of each option and consider factors such as network restrictions, coverage comprehensiveness, and out-of-pocket costs.

Ultimately, making an informed decision will ensure you have the right coverage to meet your healthcare needs during retirement. If you need help deciding, book a call with us, and we'll discuss your options.

Comments