Medicare Supplement Rate Increases in 2026

- Paula White

- Jun 6

- 4 min read

Why your Medigap premium went up — and the three practical ways to respond

Introduction

Medicare Supplement (Medigap) premiums are increasing 12% to 26% in 2026 due to medical inflation, higher utilization, and new state enrollment rules. You have three options: shop for a cheaper carrier with the same benefits, move to a different Medigap plan, or switch to Medicare Advantage. Each path has trade-offs, and timing rules apply.

If your Medigap premium just jumped, you're not alone — increases this large are happening to most carriers and most policyholders in 2026. This isn't a problem with your specific plan, and it doesn't mean you're stuck. The sections below explain what's behind the increases and walk through your options.

What's behind the 2026 Medigap rate increases?

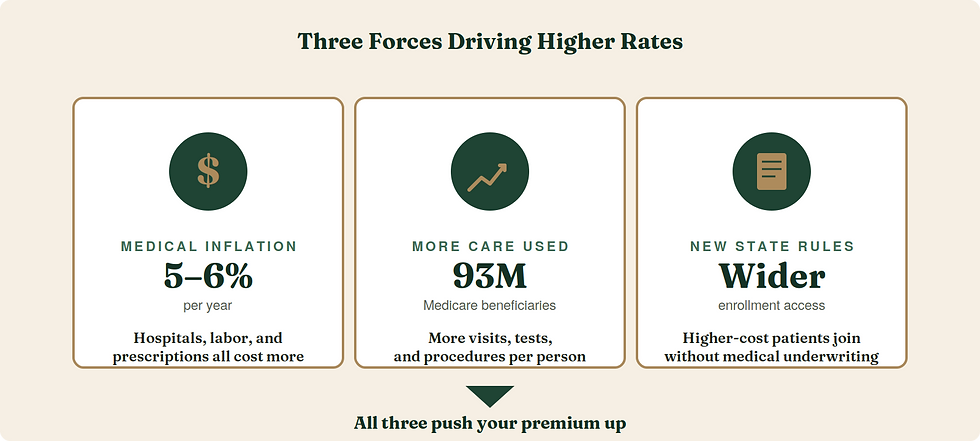

Medigap premiums are rising because of three main forces working at the same time. Health care prices are climbing about 5–6% per year, with spending per person up 6.1% in a single recent year. People are using more medical services per person as the Medicare population grows toward nearly 93 million. And some states have added rules that require Medigap carriers to enroll high-cost patients without medical underwriting, which raises claims for everyone in the plan.

On top of all that, claims have been outpacing premiums for several years. Carriers are now "catching up," and several waited too long, which is why the increases feel sudden and large.

"Five years ago, it was exceedingly uncommon to have a carrier with a rate increase of more than 10%. Now it's very uncommon to see a rate increase below 10% — and it's not uncommon to see it over 20%." — Industry executive, quoted by KFF Health News (2026)

How big are the Medigap rate increases this year?

Looking at early-2026 Plan G rate filings from the six largest carriers, approved rate increases are running between 12% and 26%. About 12 million Americans on Original Medicare carry a Medigap policy (roughly 43% of everyone in Traditional Medicare), so the impact reaches a large share of beneficiaries.

And this isn't unique to Medigap. The standard 2026 Part B premium rose to $202.90 (up from $185), the Part B deductible climbed to $283, and the Part A hospital deductible rose to $1,736. The same cost pressures hit every part of Medicare.

What can you do about a Medigap rate increase?

Option 1: Shop for a cheaper carrier. All Medigap policies with the same letter cover the exact same benefits — federal law sets them. Only the price differs from carrier to carrier. If your current carrier raised rates significantly, a competitor may offer the same plan for less. Switching usually requires answering health questions, but 16 states have a "birthday rule" that allows annual switches without underwriting.

Option 2: Move to a lower-premium plan. If you want to stay with a supplement but lower your bill, downgrading your Medigap plan is the most common move. Different medigap plans can have lower premiums but more out-of-pocket costs when you access medical care (e.g., copays, deductibles). It's a good fit for people comfortable trading a bit of out-of-pocket cost for monthly savings.

Option 3: Switch to Medicare Advantage. Medicare Advantage plans often have low or $0 monthly premiums and add a yearly cap on out-of-pocket costs. Many bundle dental, vision, hearing, and drug coverage. The trade-off is using a network of doctors and paying copays as you go. Returning to Medigap later usually requires passing medical underwriting.

How are Medigap and Medicare Advantage different?

Medigap works with Original Medicare and covers most of what Medicare doesn't. Medicare Advantage replaces how you get Medicare entirely. Neither is universally better — they suit different people. Medigap fits those who value predictability and freedom to see any Medicare-accepting doctor. Medicare Advantage fits those who prefer lower monthly costs and the safety of an annual out-of-pocket cap.

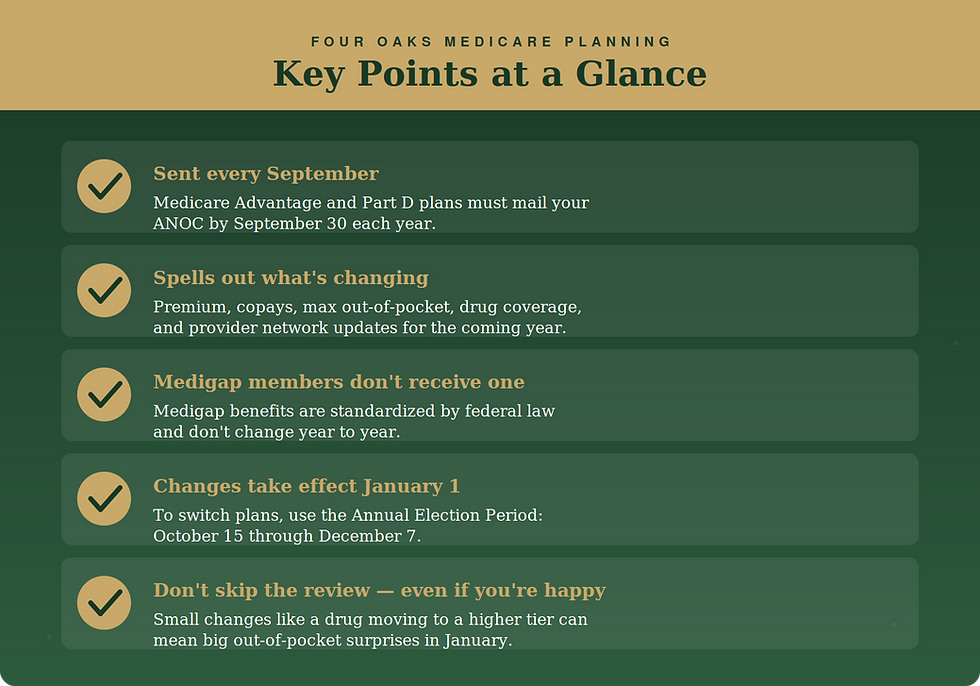

What timing rules apply when switching Medicare plans?

The most generous window is when you first enroll in Medicare — you have 6 months to buy any Medigap plan without answering health questions. After that, switching usually means medical underwriting, but several specific situations are exceptions worth knowing about:

Your original 6-month Medigap window — when you first enroll in Part B, no health questions asked.

The 12-month Medicare Advantage try-out — if MA was your first choice when you joined Medicare, you can switch back to Medigap within 12 months without underwriting.

Birthday rule states — at least 16 states allow annual Medigap switches around your birthday with no health questions.

If your Medicare Advantage plan exits your area, you typically earn a guaranteed right to buy a Medigap plan.

Specific rules and dates vary by state, so it's worth verifying your state's rules before applying anywhere.

Have Questions? Let's Talk.

If you got a rate increase letter and aren't sure what to do, that's exactly what we're here for — and our help is always free. You can reach us at 512-298-5404 · jwhite@gofouroaks.com · gofouroaks.com

DISCLAIMER

Four Oaks Medicare Planning is not connected with the Federal Medicare Program or the Social Security Administration. This article is for general educational purposes only.

Comments